RBA communications, Australian and US labour market data and technology stock weakness influencing interest rate markets.

Key points

- Australian labour market data this week is expected to be weaker than market forecasts due to payback from December strength and changes to seasonality around Christmas/New Year hiring evident since COVID. Wages growth expected to continue at a rate inconsistent with at-target inflation given weak productivity growth.

- RBA Deputy Governor Hauser noted last week, the RBA’s forecasts are conditioned on an assessment that much – but not all – of the recent pick-up in inflation was temporary. Greater policy tightening can be inferred if inflation proves persistent at the 3-3.5% rate. I expect the next interest rate rise to occur in May, barring any major overseas market or economic shocks, though longer-end rates will continue to be more influenced by US long end developments.

- US has Q4 GDP, PCE and the Fed Minutes as well as a host of Fed speakers this week. The simultaneous strength of growth and weakness in employment is unusual but reflects the divergent influences of the AI boom, tariffs and government cutbacks and shutdowns.

- Interest rate markets appear to be reacting not only to weaker technology stocks but also to some of last week’s partial data which contained indications of a soft underbelly to the US labour market. Two Fed speeches this week look at the influence of AI on the US economy and labour market.

The week in review

It’s again been quite a volatile week for markets, though not quite as wild as the previous week! The key developments since our last report on 9 February have been:

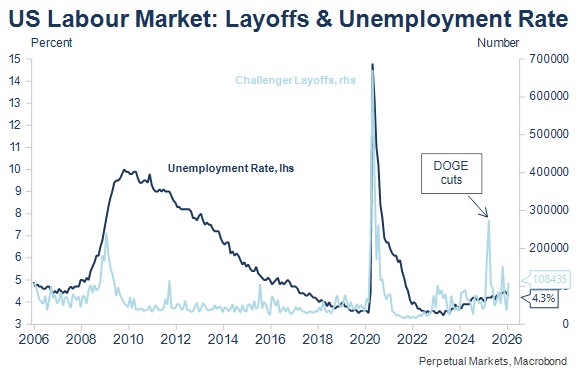

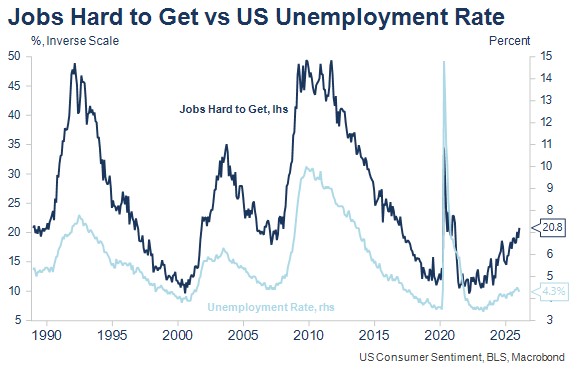

- A stronger than expected US non-farm payroll report for January. Employment growth was nearly double expectations at +130K and the unemployment rate unexpectedly fell to 4.3%. That said, at the end of the week, US interest rate markets were again focusing on weakness in technology stocks and some softer partial US labour market indicators suggesting a continuing upward trend to US unemployment is likely.

- Hawkish messaging from the RBA after the previous week’s interest rate increase. That is always the case after a tightening. More interesting was the revelation by Deputy Governor Hauser that the Bank’s inflation forecast assumes that most but not all of the recent rise in inflation is assessed to be temporary. If that doesn’t turn out to be the case, a greater need to tighten policy could be inferred than the further one and a half interest rate rises assumed in the February forecasts.

- Gold and silver prices remained very volatile, rising strongly in the early part of the week, but weakening in the latter part of the week to close slightly lower than the week before.

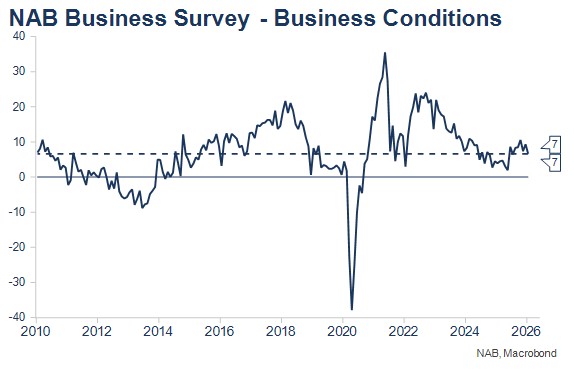

- In Australian economic data, Household Spending was weaker than expected as changed seasonality associated with Black Friday was evident, while Consumer Sentiment dropped further in February, unsurprising after the RBA increased interest rates. The NAB Business Survey was a little more of a surprise, with business conditions easing back to long-term average levels, and WA and Mining business conditions weaker. I interpret the latter as more noise than signal.

- US technology stocks remained weak, with a sharp 2.6% sell off recorded on Thursday as investors continue to have concern about the amount of debt required to finance the massive pipeline of data centre investments. Companies in the “Software as a Service” sector were particularly hard hit as there are concerns that AI can replace parts of these businesses.

RBA messaging

RBA Deputy Governor Hauser’s fireside chat last Wednesday provided a very clear expose of the Bank’s current thinking. It’s available at Fireside Chat at the Australian Chamber of Commerce and Industry (ACCI) Business Leaders’ Series | Speeches | RBA for anyone that hasn’t listened to it. For me there were two key takeaways:

The RBA is assessing much, but not all, of the recent pick-up in inflation as temporary. That along with slightly tighter policy underpins the forecast moderation of inflation back to target over the next eighteen months. The inference of course is that if the temporary assessment is incorrect, then policy will need to be tighter than the one and a half further interest rate rises that were assumed when the February forecasts were prepared, all other things being equal. I expect the next interest rate increase to be delivered in May, unless Australian data is uniformly strong between now and the March meeting, or global equity markets weaken sharply further.

The RBA is attributing the rapid about face on interest rates to three factors:

- The world economy has turned out stronger than was expected when the RBA eased last year. The AI boom was a large part of this story, but the quantum of tariffs implemented was also less than initially feared and retaliation was more limited.

- Financial conditions have been easier than expected, meaning, policy is not as restrictive as previously assumed.

- The pick-up in private demand was stronger than the RBA expected.

I remain somewhat unconvinced about the “pick-up” in inflation narrative, preferring to interpret the path of prices as having levelled out around 3-3.25% after temporarily dipping to near target in the first half of 2025. I also am not as convinced about the capacity constrained economy story, seeing this as more reflective of the still quite tight labour market, than non-labour constraints on the economy’s speed limit.

US interest rate developments key for the longer term

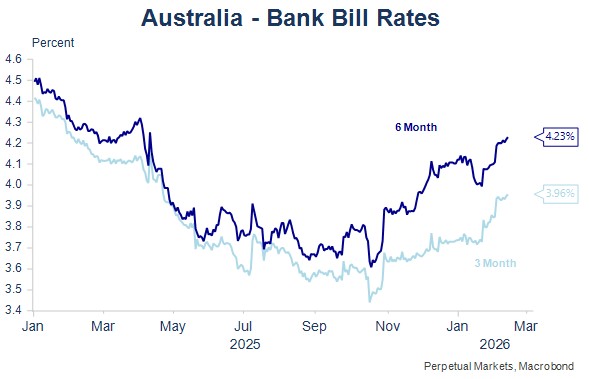

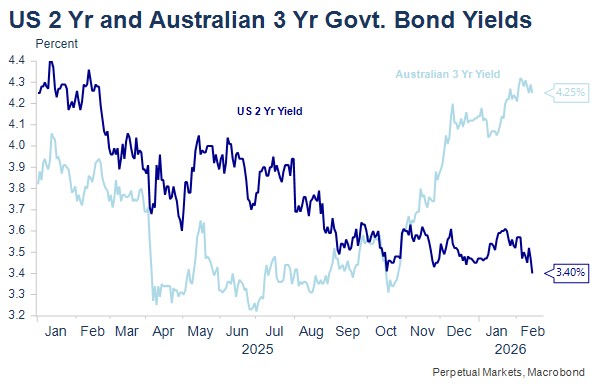

While the RBA’s thoughts and forecasts are very important for the very short end of the Australian interest rate curve, longer-term yields (and usually short end yields eventually) are driven primarily by developments in the US economy and interest rates. While 3- and 6-month bill yields drifted slightly higher again last week as markets digested the RBA’s hawkish message, US 2-year (and 10-year) yields dropped, imparting the same bias to Australian longer-term yields.

As noted earlier, and especially at the end of the week, it was the continuing weakness in selected US technology shares that was the primary influence, though a number of US partial labour market indicators continue to signal an upward drift in US unemployment.

While recent messages from FOMC members continue to signal a likely period of policy inaction in the US, tech stock weakness and partial labour market weakness remain very relevant. The AI boom provided a strong underpinning for US economic growth last year as tariffs and government cuts and shutdowns weighed on the economy. An unwind of this support would likely see current US pricing for just over two further interest rate cuts this year extend and shift forward.

More broadly, the extent to which AI displaces jobs for me remains the biggest macro question of all for interest rate managers. If the effects are large, then I’d expect a downward bias to interest rates over the medium term, though in the interim, the data centre rollout seems likely to drive strong demands for energy, water and various metals, all of which tend to be inflationary. I have also been tending to view the likely jobs impact as being in the 2+ years away timeframe, while also recommending that investors follow US labour market data closely to monitor these developments as the US seems well in advance of Australia on the AI front.

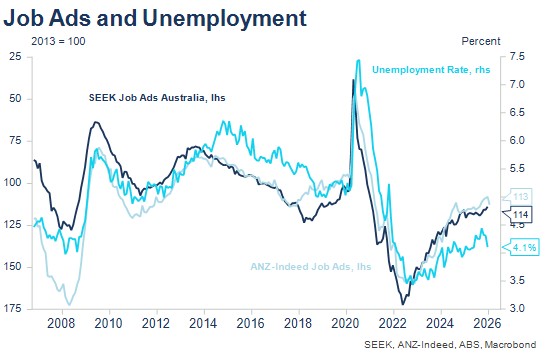

My two favourite indicators of the Australian economy

Over many years, I have been guided by the signals of two key Australian economic indicators – the business conditions measure from the NAB Business Survey and the various measures of job advertising. Both are extremely reliable indicators of the trend for the Australian economy, with labour market indicators particularly useful at times like the present, when there are many different influences acting upon the economy.

Looking at current trends, we can see only a very slight downward trend to job ads over the past eighteen months, which is consistent with only a slight upward bias to the unemployment rate, while Australian businesses continue to report operating conditions that are around or slightly above long-term averages. That’s a picture of an economy currently growing around trend, with little significant pressure on the unemployment rate.

Short-term market drivers and the economic calendar this week

This week the data focus will be on Australian wages and employment and unemployment data. It’s likely that wages growth will continue to run at a 3.25-3.5% rate, too high to be consistent with 2.5% inflation when productivity is running around zero. Last month, employment surprised sharply to the high side with a +65K print and a very surprising drop in the unemployment rate to 4.1%. I’d expect a weak employment reading as payback to December strength but also as a result in changes to employment practices over December and January that have been evident since COVID. It would be surprising if the unemployment rate did not reverse at least some of last month’s fall.

The main short-term drivers of Australian interest rate markets however are expected to be developments in US tech shares, with any further weakness likely to extend – and bring forward - pricing for further US interest rate cuts. The US calendar has the Fed Minutes and a raft of Fed speakers – including two with interesting speech topics relating to the impact of AI on the US economy and labour market. Late in the week there’s the first estimate of Q4 US GDP and the latest monthly PCE inflation estimate. All of the Fed Minutes, GDP and the PCE are likely to be less relevant than normal if technology shares continue to fall.

Economic Calendar – key Australian and US events this week

- Tuesday 17 February – RBA Minutes.

- Wednesday 18 February – Wage Price Index (Nov); RBNZ Policy Decision, (overnight) Fed Minutes, Durable Goods Orders, Capacity Utilisation.

- Thursday 19 February – Labour Force (January), Initial Jobless Claims.

- Friday 20 February – RBNZ Governor speech; (overnight) Q4 GDP (first estimate), Private Consumption Expenditure deflator.

- Speeches from the Fed’s Bowman (Monday), Barr and Daly (Tuesday) – both interestingly talking about AI and the economy/labour market, Bostic, Kashkari and Goolsbee (Thursday) and Logan and Bostic (Friday).