Perpetual Markets Economics and Interest Rate Commentary – 23 March 2026

1990 Gulf War playbook continues to hold. Trump gives Iran 48 hours to re-open the Strait of Hormuz, but market pricing reflects concerns over a longer conflict. Central bank commentary more hawkish and short-end yields rise sharply.

Key points

- Markets continue to follow the 1990 Gulf War playbook with oil prices continuing to rise, equity markets to weaken and bond yields higher as the Strait of Hormuz, through which 20% of global production is shipped daily, remains closed.

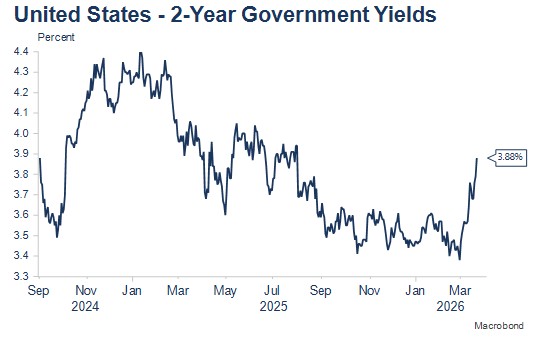

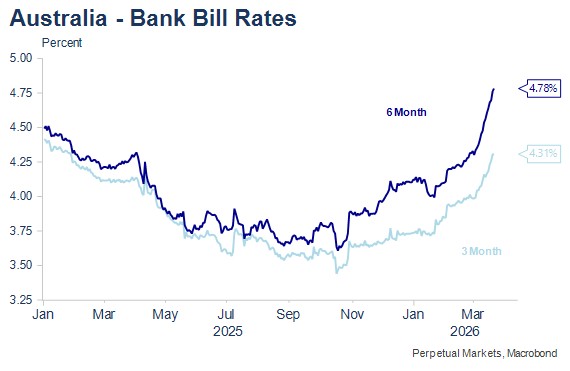

- Australian and US short end yields rose sharply this week. In 1990s, central banks focused on rising unemployment as economies entered recession. For now, with unemployment relatively low in the US and Australia, above-target inflation is the focus. That message was reinforced by the RBA’s second consecutive interest rate rise at the March Board Meeting and more hawkish commentary emerging after other central bank meetings last week. Markets are now pricing a 40% chance that there is one US interest rate rise by October from pricing two cuts by the end of 2026, two weeks ago!

- The length of time the Strait of Hormuz remains closed is key for markets. If there is a very extended closure – eg three to six months – oil prices are likely to rise significantly further (AI estimates $230-300pb oil is required to destroy 20% of world demand, higher than my intuition of $180-200pb). Either of those price levels sustained for three to six months would likely be sufficient to tip the Australian and world economies into recession.

- Likely reflecting the increasingly severe oil price situation, President Trump announced over the weekend that Iran had 48 hours to reopen the Strait, otherwise the US would begin bombing Iran’s power stations.

- Australia remains heavily reliant on imported petrol and diesel. In the event of the extended closure of the Strait of Hormuz scenario, it’s quite likely that fuel supplies in Australia will be interrupted, which could create some economic activity “stoppages” as occurred during COVID lockdowns. Data prints like recession, but activity can quickly return once the stoppage clears.

- Some of the international data to be released this week will reveal the first impacts of the fuel crisis on activity and inflationary expectations. The February Australian CPI would normally be very market moving, but like other data has been overtaken by March’s fuel price rise. Australian petrol prices already appear set to rise 30% m/m in March. With a 3.4% weight in the CPI, that will add one full percentage point to the headline CPI in March and will bias the trimmed mean CPIs for March and the March quarter higher, meaning another 0.9% or 1% q/q figure is likely.

- That would ordinarily be enough to see an almost automatic tightening by the RBA. However, the first-round effects of oil price shocks are typically looked through by central banks. The policy reaction will depend on the starting point for policy (expansionary, neutral or restrictive), the impact on inflationary expectations, the risks of second-round inflationary impacts (it’s a bad time from a national wage case setting perspective for Australia to experience a large oil price spike), and on any offsetting growth impacts. The latter is different to the COVID experience (as is the behaviour of oil prices), when supply chain disruptions coincided with very strong demand.

- With the Board having moved in February and March and the May Budget expected to incorporate spending cuts, there is the option to sit out the May meeting to assess the situation better, though the clear inflationary pressures from oil may see the Board prefer to have interest rates closer to a pre-crisis slightly restrictive level. For now, I’m still punting for a May pause. The nearly three rate hikes now priced for Australia by the end of 2026 also seems excessive, particularly if oil prices remain very high.

The week in review

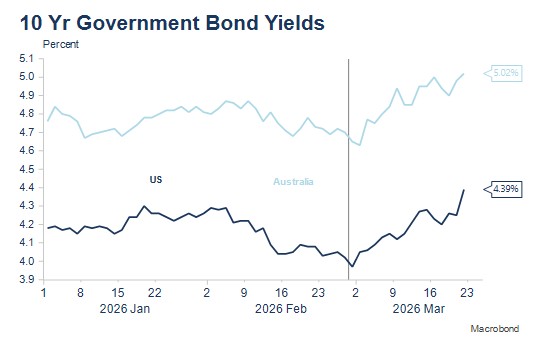

The markets continued to follow the 1990 Gulf War playbook, with oil prices continuing to rise as the Strait of Hormuz remains closed and an early end to the conflict does not currently seem in prospect. Likewise we’ve seen longer bond yields rising on oil-related inflationary concerns and share markets softening on expectations of slower economic growth from higher oil prices and interest rates.

Like last week, developments were mostly, relatively orderly, though short end yields have risen sharply as central banks signalled concern about inflation and markets priced likely official interest rate increases. The RBA as expected increased interest rates for the second consecutive month.

The repricing of short ends was dramatic in the US (and also in the UK), where markets are now pricing a 40% chance of an interest rate increase by October, compared to pricing one further interest rate reduction a week ago, and two cuts by the end of the year two weeks ago. The FOMC Meeting saw members shift their interest rate expectations moderately bearishly (less cuts seen), though the median expectation remained for one cut this year and one next year. No dot point anticipated an increase during 2026. 2-year yields rose 18bps over the week.

Australian shorter-dated and longer-dated yields have also risen sharply, with markets now effectively pricing three further interest rate rises by the end of 2026. That degree of tightening, together with an extended period of current or still higher oil prices, would see markets anticipating recession and lower interest rates further out.

The chances of recession

In considering the chances of an Australian or global recession, there remain two important considerations. Chiefly, these are how high oil prices rise, and more importantly, the length of time that oil prices stay elevated. Another important consideration for businesses is the potential that fuel supplies might not be available (at any price), something that there have already been reports of in some regional areas of Australia. The latter is akin to both the supply chain disruptions that characterised many goods during the COVID period, but also to the lockdown interruptions to activity, with fuel obviously a very central component of virtually all aspects of the economy.

Historically oil price rises of 50-70% that are sustained over a one to two quarter period have often been associated with global recession, constituting both a very significant and importantly, sustained price shock.

The size of the oil price rises so far experienced is in that 50-70% range, however, these higher prices have only been experienced for around three weeks. The ultimate duration of higher oil prices depends on two factors: (i) the time the Strait of Hormuz remains closed; and (ii) the damage inflicted on the region’s energy infrastructure during the conflict. A quick re-opening of the Strait of Hormuz would likely see oil prices drop sharply. An extended closure could see much, much higher oil prices, as markets would push prices up high enough to ration or “destroy” an equivalent amount of demand (as I noted last week, AI suggested prices in the $230-300pb range would be required to destroy this much demand).

The week ahead: Economic Calendar – Key Australian and US events

Monday 23 March – (overnight) Global S&P composite PMIs (March); these should show an initial negative reaction to higher oil and gas prices but will only reflect part of the March oil price rise impact.

Tuesday 24 March – AOFM tenders $1bn 3.75% 2037 bond. Barr speech.

Wednesday 25 March – Australian CPI (February); (overnight) IFO (March). Miran speech.

Thursday 26 March – RBA Assistant Governor Kent Speech; (overnight) Cook, Barr, Jefferson, Miran speeches.

Friday 27 March – (overnight) University of Michigan Survey (March); speeches from Daly and Paulson.

February and early March economic data remains mostly irrelevant at the present time, as it pre-dates the rapid escalation in oil prices this month. As such, most data – including Australia’s February CPI on Wednesday – is useful mainly as a baseline from which to overlay the current oil price shock effects.

That said, there are a number of international stats this week that will begin to reveal the first impacts, with the German IFO, various S&P global composite PMIs on Tuesday, and University of Michigan consumer confidence and inflationary expectation readings, all for March, being released. The data will invariably show weaker growth or growth expectations and higher inflation expectations, but at this stage will only capture part of the effects of oil price movements during March.

Wednesday’s February Australian CPI also pre-dates the very large rise in petrol prices. The 0.3-0.4% m/m increases being recorded for the large housing components tends to mostly generate 0.3% m/m increases for the trimmed mean – the current implied expectation for this month’s result (market expectations are for 3.4% y/y for the trimmed mean and 3.8% y/y for headline). Importantly, the very large increase in petrol prices in March (already in the order of 30% m/m), should bias the monthly and quarterly trimmed mean readings higher for March and Q1.

There are two senior RBA official appearances, with Chris Kent’s speech more likely to be of relevance for monetary policy, but usually more market focused. In the US, a host of FOMC speakers’ opinions will be closely examined as the market begins to price the next move in US interest rates as being an increase.