Perpetual Markets Economics and Interest Rate Commentary – 30 March 2026

Observations on the first four weeks of the conflict

Key points

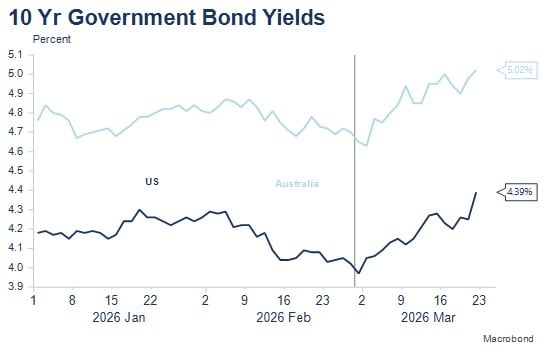

- The 1990 Gulf War “playbook” remains in force with oil prices and bond yields remaining elevated and equity markets continuing to weaken.

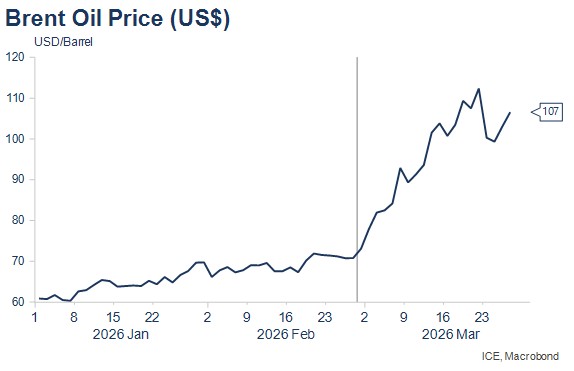

- How long the Strait of Hormuz remains closed appears the biggest short-term issue. An extended closure would likely see oil prices rise very sharply to “destroy” the near 20% of oil demand affected by the closure. Market pricing at around $110pb for Brent crude oil does not significantly discount that possibility.

- The US is reportedly increasing the number of troops in the region. My observation is that troop and armament build-ups have typically preceded escalation rather than de-escalation in recent times (e.g. Russia/Ukraine, US/Iran).

- Very few of us have any idea how long this conflict will last and therefore the ultimate impact on economies, inflation and markets. Consequently, we are left creating and managing scenarios and probabilities. In the near-term, it’s clear the world is dealing with a significant inflationary shock, that will be negative for much economic activity, while it continues. The shock (and oil prices) could unwind relatively quickly if the conflict is resolved, though it could equally escalate significantly if the Strait of Hormuz remains closed for an extended period. The prospect of limited oil supplies causing interruptions to economic activity is also relevant (it was noticeable that many service stations in Sydney had limited supplies on Sunday).

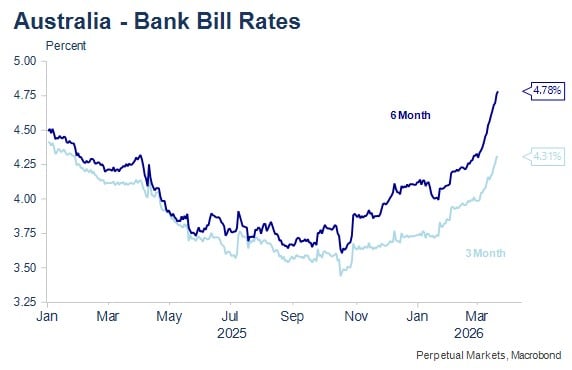

- Central banks globally are speaking from the same book, noting that it is appropriate to look through the first-round impacts on inflation. Policy makers will be concerned with second-round impacts; the prospect that longer-term inflationary expectations adjust higher, that wages rise, or that firms’ pricing behaviour adjusts. That suggests the risk that policy should be set in a more restrictive manner or not eased further in the near term while the crisis sustains or extends. US markets continue to factor only a small probability of the next move in US interest rates as being a rate rise, though this is a significant change on the pricing of easings just a month ago. Australian markets are discounting a high probability of a further interest rate rise in May, but a full further rate rise is not factored until June. The markets nearly fully price three interest rate rises by November - that seems a little aggressive given activity will also be impacted by high oil prices.

- The AI investment boom has not gone away - nor the possible negative longer-term implications of this boom for employment. In the short term, the data centre rollout also adds to inflationary pressures, with reports of potential capacity pressures in semi-conductors, electricity, water and selected metals (including copper).

- Australian and US data mostly pre-date the latest developments, though this week, the US publishes the Manufacturing ISM and Non-Farm Payrolls for March. The ISM data may show a taste of what is to come, particularly on pricing and supply chains, though the labour market survey likely was too early in the month to capture much impact. February and early March data is still most useful as a baseline to overlay the current emerging shock.

- There is increasing discussion of stagflation. That term has been used incorrectly in recent years to describe the recent period of elevated inflation and slower (but not very slow) growth. The important missing ingredient (thankfully) from the stagflation years of the early to mid-1970s has been very high unemployment. A very extended oil price shock (Strait of Hormuz closure) may bring about an outcome with more similarities to those stagflation years, with inflation-targeting central banks unable to support economic growth or labour markets if inflation and inflationary pressures remain elevated.

The month in review and observations to date on the conflict

It’s been just over four weeks since the US and Israel began military operations against Iran. This month in review contains observations about the key issues both to date and in prospect:

- Markets continue to follow what I refer to as the 1990 Gulf War playbook, with oil prices rising sharply, bond yields rising on related inflationary concerns and equity markets dropping as the risk of slower growth/recession rises from higher oil and bond yields.

- Somewhat different to 1990, markets have removed easing expectations or priced in the prospect of higher short-term interest rates in the next six to twelve months and central bank communications have turned hawkish. While central banks will, as usual, look through the first-round price effects of the oil price rise, they will seek to prevent any second-round inflationary effects, including impacts on inflationary expectations.

- This likely reflects the long period of above-target inflation already experienced, and in truth is similar to the 1990 Gulf War playbook. Then central banks also focused on the key domestic fundamental, which was rising unemployment rather than inflation as global economies entered recession. Monetary policy was eased throughout the conflict in spite of higher oil prices initially.

- The key development has been the effective closure of the Strait of Hormuz. Around 20% of the globe’s production of oil and LNG and around 10% of global supply of fertiliser and petrochemicals used in the production of plastics flow through this waterway. This constitutes another very significant supply shock to the world economy.

- Damage to energy infrastructure is also important, but not as significant for oil prices in the short term as the closure of the Strait of Hormuz, given the volumes of product that flow through the Strait each day. Logically then, the reopening of the Strait of Hormuz can improve oil supplies and lower prices quite quickly, though damaged infrastructure should mean prices do not fully return to pre-conflict levels for some time, in the absence of slower economic growth.

- My prior is that a sustained oil price of US$125-150 per barrel would likely be sufficient to cause global recession, these levels marking the 50-70% y/y oil price rises that have typically preceded oil-price-related economic slowdowns. Different to previous times, the AI-boom and massive data centre rollout globally will continue and could mean that higher than normal oil price rises might be required to cause recession.

- An extended closure of the Strait of Hormuz would see oil prices need to rise sufficiently to “destroy” 20% of global oil demand. My guess was that would be somewhere around US$200 per barrel, though AI (Co-Pilot) suggested US$230-300 per barrel would be required, after consulting various previous analyses estimating global oil demand elasticities.

- Either way it’s much higher oil prices than anything we have seen to date, which allows us to infer that current market pricing is still factoring a relatively quick end to the conflict.

- The comments so far have focused on the price effects of the conflict. Equally important is the prospect that supply might be significantly affected and fuel supplies might not be available at virtually any price in the short term. This has the potential to create the same interruptions to activity that occurred during COVID. These had some of the characteristics of recession but ultimately proved mostly short lived. That’s not to say that they are not important and will no doubt add pressure to already-impacted companies’ cash flows and resources.

- Petrol prices appear likely to average 30% higher in March than in February. This will add around one full percentage point to the headline CPI in March, but a lesser amount to headline CPI in the March quarter (the average rise for the March quarter is around 4.5%, which would add 0.15 percentage points to the March quarter headline rate). Larger rises will be recorded in the June quarter. Importantly, the March quarter trimmed mean rate will likely also be biased slightly higher, though the RBA will look through this effect.

- Economic data released over the past month is somewhat but not completely irrelevant, given it pre-dates the very large oil price rises that have occurred through March. The data is useful as a baseline to overlay the recent rise in oil prices. Importantly, from the point of the RBA’s inflationary concerns, the unemployment rate in February rose to 4.3% from 4.1%, while the monthly trimmed mean CPI was 0.2% (down from 0.3% m/m in January). I note that for the past three quarters - for some reason I have yet to figure out - the trimmed mean in the first month of the quarter has been high and the second month of the quarter much lower.

The Outlook

In the short-term, this appears to depend most crucially on how long the Strait of Hormuz remains closed and in the medium-term, the damage done to oil producing infrastructure in the region. While the Strait of Hormuz remains closed, I expect oil prices to continue to rise very sharply to recession-inducing levels well above US$150 per barrel. And while central banks are currently talking tough on interest rate increases, this scenario would likely ultimately constrain the upside for interest rates and bond yields, given the impact on activity and unemployment.

One possibility that deserves consideration is a period of stagflation. This term has been used loosely - and I would argue incorrectly - in recent times when inflation has been quite high. However, the economic conditions in recent years, despite having temporarily high inflation don’t fit with the stagflation experience of previous oil shocks, most importantly because unemployment rates have remained very low around the world. Growth has also been moderate rather than very weak and inflation only temporarily very high. It is possible that an extended supply side shock that pushes oil prices much higher for a long period, could give rise to a recession followed by another period of stagflation. This would likely be negative for longer-term bond yields and would be quite difficult for central banks to navigate as their unemployment and inflation objectives would be in conflict.

It’s important not to forget about the AI investment boom and associated huge data centre roll out. In the short term, this adds to inflationary pressures via extra demand for semi-conductors, electricity, water and certain metals, including copper. Longer-term, the implications for employment remain uncertain.

In the first instance, the market needs to trade the inflationary consequences and pressures of higher oil prices and the data centre rollout, while being alert to the tipping point where high oil prices switch from being an inflationary concern to causing recession. Under either scenario, increased pressures on consumers’ and business’ budgets and cash flows, will likely weaken equity prices and credit, until such time as there is a peaceful or military conclusion to the situation. That timing remains very unclear, though several US officials have suggested that the US is close to achieving its objectives. This remains to be seen, though it’s interesting that the US is significantly increasing the number of marines deployed to the region. Recent troop and weaponry buildups have tended to precede escalation rather than de-escalation.

Economic Calendar – key Australian and US events this week

It’s still the case that February data is useful mainly as a baseline to overlay the latest Iran oil shock, while March data will likely only partially capture these effects. There are two always important US data points released this week (non-farm payrolls and the Manufacturing ISM), that will be watched closely to see the extent to which price expectations might rise and to which activity might already have slowed. There are also two very senior Fed members (Powell and Williams) speaking overnight Monday and early on Tuesday, whose words will be important in giving extra insight into how the Fed might respond to the current shock. An AI summary of central bank statements and speeches in the past few weeks confirms the common themes have been to look through the first-round impact of the shock, but to set policy to limit second-round impacts on inflation, inflationary expectations and pricing behaviour. That’s negative (bearish) for short-term interest rates given the current magnitude of oil and LNG price rises unless resolved relatively soon, though of course, we have little guide as to how quickly the situation may resolve.

Monday 30 March: (overnight) Fed Chair Powell speech (1.30am Sydney time Tuesday); Fed Williams speech (7am Sydney time, Tuesday).

Tuesday 31 March: AOFM tenders $1bn 3.75% 2037 bond. (Overnight) US Job Openings (6.89m expected) after 6.95m in January - note this is still only February data on the US labour market.

Wednesday 1 April: Building Approvals (February) - the market expects a 6% rise after a 7.2% decline in January (the risk is much stronger for this volatile series). (Overnight) US Retail Sales (February); Manufacturing ISM (March). The latter will be interesting as it may begin to show some impacts on activity and price expectations. Economist forecasts expect an unchanged index but slightly higher prices - presumably the April reading will have much larger moves.

Thursday 2 April: Job Vacancies (3 months to February) - again this data provides a baseline for how the Australian labour market was faring ahead of the Iran conflict. The RBA of course continues to describe the labour market as a little tight, which means unemployment is lower than is consistent with at-target inflation. (Overnight) Challenger Layoffs (February) - previous January was a relatively low 48,307.

Friday 3 April: Good Friday - Australian markets closed. US non-farm payrolls (March). A 60K increase in employment is expected after the 92K fall in February. The latter was heavily weather affected due to a large winter storm, providing significant risk of such a counter-trend bounce-back. It’s very likely however that payrolls will resume their weakening trend, while oil prices remain very elevated. Markets expect an unchanged unemployment rate of 4.4%. This rate can be expected to rise in coming months.

Monday 6 April Easter Monday - Australian markets closed. (Overnight) US Non-Manufacturing ISM.

The National Wage Case

The Australian media reported late last week that the Government supports an economically+ sustainable real wage rise being delivered for Australia’s lowest paid workers in the upcoming National Wage Case (the minimum wage adjustment). While I almost always support minimum wage rises, at face value this recommendation does not seem wise. The CPI will be significantly boosted by oil prices in coming months, with the headline rate likely to be around 5% y/y in March. This rise might be temporary and quickly reverse, in which case delivering a real wage rise off a temporarily inflated base, would be an unreasonable impost on business.

In my opinion, it would be better for the Commission to either delay its decision a little and reconvene in a few months’ time once the duration and extent of the current shock is hopefully known a bit better. The government’s recommendation - if followed - would likely have the unwanted effect of placing monetary policy and wages policy in contradictory positions, with a real wage rise from a possibly temporarily elevated base likely to add to above-target inflationary pressures as a further inflationary shock develops.

Chart Round-up