Perpetual Markets Economics and Interest Rate Commentary – 1 June 2026

Peace deal close but unsigned. Very big week for Australian and US data and RBA events. Minimum wage deal important.

Key points

- Despite reports last week of an MoU to end the war and reopen the Strait of Hormuz, a deal has not yet been signed. If agreed, interest rate markets should be able to rally a bit further as oil market pricing normalises, before the re-establishment of a stronger economic outlook, particularly in the US, imparts a medium-term slow, bearish tilt to interest rate pricing.

- It’s a huge week for Australian and US data and events, though a peace deal would effectively override any data.

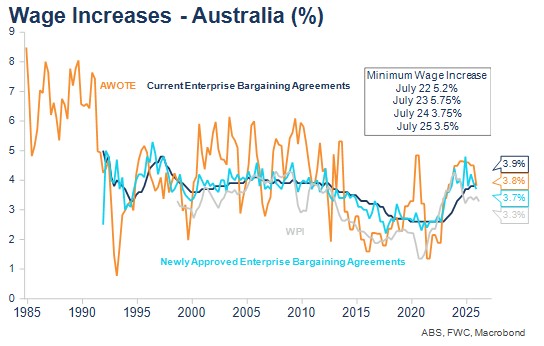

- In Australia, a Minimum Wage Deal of 3-3.5% or below would be helpful for the RBA, while a higher outcome would make it harder to deliver inflation at the 2.5% target. Speeches from Board Member Harper and Deputy Governor Hauser will be important, as will the Governor’s appearance at a Senate Economics Committee. Q1 GDP is very dated but seems at risk of adding to the RBA’s narrative of a capacity-constrained economy, with little danger of much downside to the market forecast of a 0.5% quarterly growth rate.

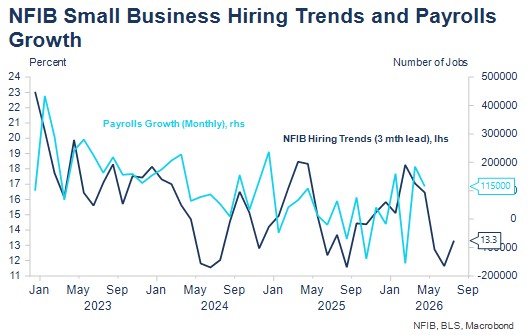

- In the US, the ISMs and labour market data are the focus. These are likely to show the continued inflation pressures that have seen FOMC participants remove any thoughts of near-term easings, but are expected to also show the US labour market remains somewhat fragile, producing only very slow employment growth. NFIB data suggests risk of slower employment growth over the next few months, but I’m tending to think that might be next month.

Middle East developments

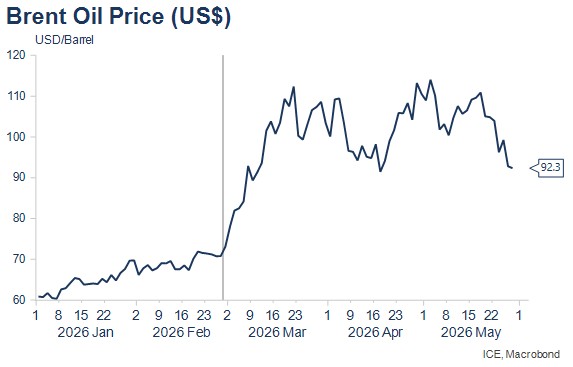

It has been another week with greater optimism about a peace agreement being signed but still with very few ships transiting the Strait of Hormuz. The rumours of both parties being close to a deal that circulated last weekend contributed to lower oil prices throughout the week, assisted by news later in the week of a proposed Memorandum of Understanding. The latter would extend the ceasefire for 60-days and provide the framework for future nuclear negotiations, the reopening of the Strait of Hormuz, and the lifting of the shipping blockade and other financial sanctions. That MoU has yet to have been agreed by President Trump and over the weekend, he is reported to have first said a deal was “imminent” on Saturday and then directed negotiators “not to rush into a deal” on Sunday. Oil prices have risen US$1.50pb or 1.7% in weekend trading on IG Markets but remain around US$10pb lower than last weekend.

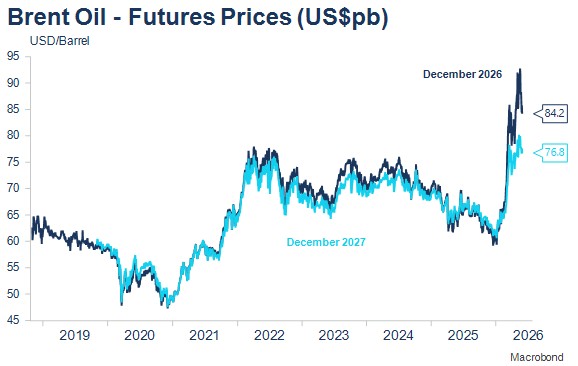

Looking ahead, if a deal can be reached, the key focus for world markets will be on how quickly oil capacity and shipping flows can be restored to pre-crisis levels. Markets are likely to focus on transit figures for the Strait of Hormuz and the behaviour of forward oil prices. There were declines in forward oil prices over the past week, but unsurprisingly these were only slight given the continued effective closure of the Strait of Hormuz.

![]()

Interest rate market developments and pricing

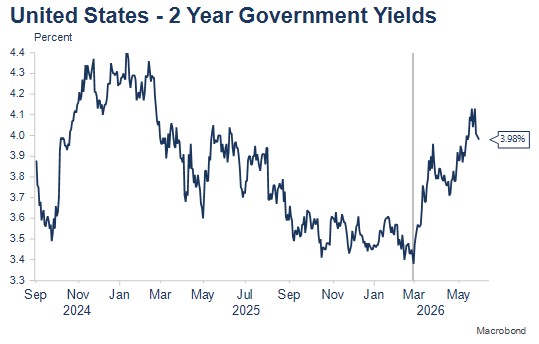

It was a more positive week for US interest rate markets, with lower yields underpinned by the decline in oil prices over the week, and news that the April PCE deflator came in at a lower than expected 0.2% m/m. This saw markets reprice the extent of potential US interest rate rises from nearly one and a half 25bps rate rises by April next year at the time of writing last Monday, to just under one rate rise by April next year. The 2-year bond yield declined 15bp over the week as a result.

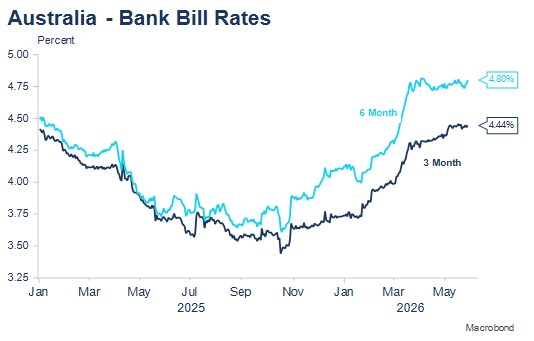

Australian longer bond yields fell over the week, though not as significantly as US bond yields, even though Australian core inflation also printed slightly lower than expected at 0.3% m/m in April. That’s still too high as the monthly core rate of inflation needs to average marginally above 0.2% to annualise at the RBA’s 2.5% target. However, coming on the heels of the rise in the volatile unemployment rate to 4.5% in April, this has seen the market effectively reduce the chance of a rate rise at the RBA’s mid-June board meeting to zero.

This is in line with guidance that the three successive interest rate rises at the start of the year had created space for the Board to monitor developments in the economy, inflation and the Middle East for a time. Australian market pricing now reflects around a 70% chance of an additional interest rate increase before the end of 2026, around half the pricing that existed prior to the release of the April unemployment figures. Lower oil prices would also have been helpful.

The week ahead – key Australian and US events

It’s a very big week ahead with the Fair Work Commission’s decision on the Minimum Wage, three RBA “events”, the usual beginning of month deluge of US labour market data culminating in Friday’s non-farm payrolls release, the Manufacturing and Services ISMs, the Beige Book, a host of Fed speakers, and the release of Australia’s Q1 GDP (probably the least exciting of all the events to me). And of course, there might be a peace agreement, which is more important for the course of inflation, economies and monetary policy than any of the other events. Current economic data becomes far less relevant if a peace deal is inked.

I’ll also keep a weather eye on today’s Melbourne Institute and ANZ Job Ads data as the former is the earliest indication of Australian inflation each month and the latter, a reliable lead indicator of the trend in the unemployment rate. Job ads softened a little in April, but the data can be impacted by Easter, school holidays and ANZAC Day timing, and hasn’t been signalling any significant change in the unemployment rate in recent months, unlike the 4.5% unemployment rate recorded in April, which I would caution looks suspicious to me.

The Fair Work Commission Minimum Wage Decision is important. Despite the RBA narrative that the economy is broadly capacity constrained, I continue to assess that as more backfitting the economic data to the inflation outcomes rather than genuinely reflecting broad-based capacity constraints. There is some evidence of constraints in the labour and housing markets, though the latter appears to be easing.

Recent FWC minimum wage decisions have granted above inflation wage rises in essence to catch up for previous inflation outcomes. That’s likely contributed somewhat to above target inflation outcomes. A 3-3.5% wage increase would likely be just affordable, given relatively low productivity growth, but won’t be helpful from a broader inflationary perspective as small businesses also confront (at least temporarily) higher transport costs. An outcome above 3.5% would create more work for the RBA. There had been some discussion about delaying the decision until the Middle East situation became clearer, which made sense to me, though this week’s announcement suggests this has not occurred. Perhaps the decision might incorporate some adjustment or delay?

There are three RBA appearances of note; RBA Board Member Ian Harper speaks on Current Economic Conditions and the Economic Outlook on Tuesday. He used to be very open with his views in the media, so I’d expect very policy relevant commentary, with most interest on the prospect for further interest rate rises beyond the June meeting, where no change is expected. The RBA Governor also appears before a Senate Committee, while the RBA Deputy Governor has a fireside chat on Friday afternoon with Sky News and The Australian. The Deputy Governor has tended to be quite open with his views in recent appearances, so markets will also follow this appearance closely.

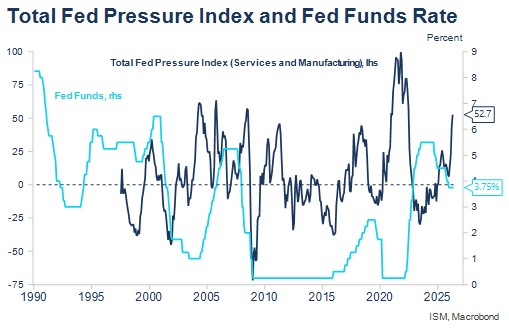

Overseas, there’s my favourite ISM indicators out of the US tonight and on Wednesday. The components sensitive to inflation have risen sharply, signalling markets should be pricing risk of higher US interest rates. Importantly, this trend was beginning to emerge, though not to the same degree prior to the US Iran conflict. The comments from respondents in the ISM surveys are always must-reads as a near real-time reflection on developments in the economy, as is the Beige Book. Interestingly, in recent times, the ISM comments have mostly reflected a stronger US economy, albeit with significant inflationary pressures.

The US labour market remains the main factor preventing a more significant sell off in US interest rate markets. Employment growth has remained very slow. Somewhat unusually, a significant reduction in illegal immigration means slow employment growth is consistent with unchanged unemployment. The doves on the FOMC continue to see this as a fragile labour market condition, though thought leaders on the Committee, like Governor Waller, have deferred calls for lower rates in the face of greater inflationary pressures and less concerning labour market data in recent months. The NFIB Hiring Trends indicator suggests there may be some downside risk to payrolls over the next few months.

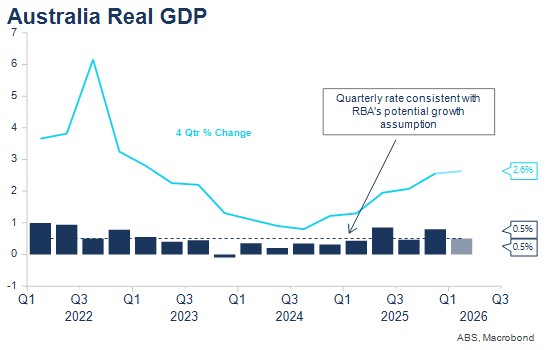

I have deliberately left Australia’s Q1 GDP release until last. This reflects a personal bias that the data is not especially relevant given the significant delay in its publication: we are already two months into Q2, and of course this time around there was a very significant development in the third month of Q1, which will be more influential for Q2’s data.

Ahead of Tuesday’s Net Exports, Government Spending and Company Profits data, the market is looking for a 0.5% q/q and 2.6% y/y outcome; the former around the RBA’s estimate of potential growth, the latter, cumulatively above potential and under the RBA’s narrative, adding to capacity constraints.

I’m a fan of hours worked as an indicator of GDP. Hours worked rose 0.9% in Q1 after a 0.4% increase in Q4. That suggests little risk of a significant downside to the market’s 0.5% forecast, with the most likely revision likely to come from stronger investment spending or less negative net exports.

Monday 1 June: Melbourne Institute Inflation Gauge (May); ANZ-Indeed Job Ads (May); (overnight) Manufacturing ISM (May).

Tuesday 2 June: Fair Work Commission Minimum Wage Decision (10am); RBA Board Member Harper speaks on Current Economic Conditions and the Economic Outlook (10.30am); Building Approvals (April); Net Exports (Q1); (overnight) JOLTS (May).

Wednesday 3 June: GDP (Q1); ISM Services (May); Beige Book.

Thursday 4 June: RBA Governor Testimony to Senate Economics Legislative Committee (3pm); (overnight) Challenger Layoffs (May).

Friday 5 June: RBA Deputy Governor Fireside Chat (2.35pm); (overnight) Non-Farm Payrolls (May). Median (+89K after +123K). Unemployment (4.3%, unchanged).

There is also a large program of Fed speakers including Waller, Powell, Kashkari, Hammack, Barr, Logan, Barkin and Daly before the Fed enters its communications blackout ahead of the June 16-17 FOMC Meeting, the first under new chair Warsh. That press conference should be most interesting viewing.

Outlook

I’m still an optimist on a peace deal being signed soon, though each week that passes reminds me I need to assess this “soon” in an economic timeframe (1-2 months); not my normal “soon” of 1-2 days or a week. Should this prove to be the case, my expectation remains that the world economy, after a period of oil market normalisation over some months, should be able to re-establish the pre-Iran conflict economic outlook.

That outlook was more favourable for US economic growth as the AI investment boom continued but also contained some inflationary pressures that were emerging even ahead of the Iran conflict. These were evident in ISM prices paid and in comments and pricing suggesting potential shortages in semi-conductors and copper, as well as demand for power and water as data centres are rolled out globally.

To me, these pressures suggest US markets should not return to pricing interest rate cuts any time soon, with the next move in US interest rates more likely to be a rise. At the same time, the medium-term implications of AI for employment, inflation and interest rate policy in the 2+ years’ timeframe remain uncertain, with clear downside risks.

Australian interest rate markets as usual, are likely to take their directional cues from the US. I’d expect interest rate markets to rally in the near-term, unwinding some of the Iran conflict increase in yields if a peace agreement and Strait of Hormuz reopening occurs soon. But I’m inclined to be a medium-term seller after this expected shorter-term favourable move and my base case is of the emergence of a slow tightening cycle.